Drag. Drop. Deploy Intelligence: Custom Research With Wokelo’s Agentic Workflow Builder

Reading Time: 4minutesIn investment and strategic advisory, no two projects are ever truly alike in their demands. From rigorous diligence reports, investment memos aligned to a thesis, or an executive brief on recent transactions – standardized templates cannot cover all scenarios. Building polished deliverables that meet the bespoke standards of each client or stakeholder translates into overstretched analyst hours. And even then, the process looks drearily similar and repetitive – hunting down information across multiple sources, to stitching together data pulls, and building narratives. Wokelo’s Agentic Workflow Builder changes that — puts an intuitive drag-and-drop canvas in your hands to design and deploy custom research agents for any use case in minutes. You can now customize and automate research, analysis, and output generation, at-scale. What you get is a pre-trained, domain-specialized agentic workflow that: Wokelo Workflows: Custom, Composable, Ready for Action With Wokelo, you’re not confined to our library of predefined, curated workflows. Instead, you can create your own research agents — reusable, modular, and tuned to your exact process. Unlock endless use cases meeting search and intelligence needs of every team: Your research, your way Combine the sophistication, ease, and reliability of Wokelo’s agentic AI platform, with the output type and […]

Reading Time: 4minutesIn investment and strategic advisory, no two projects are ever truly alike in their demands. From rigorous diligence reports, investment memos aligned to a thesis, or an executive brief on recent transactions – standardized templates cannot …

Reading Time: 4minutes

In investment and strategic advisory, no two projects are ever truly alike in their demands. From rigorous diligence reports, investment memos aligned to a thesis, or an executive brief on recent transactions – standardized templates cannot cover all scenarios.

Building polished deliverables that meet the bespoke standards of each client or stakeholder translates into overstretched analyst hours. And even then, the process looks drearily similar and repetitive – hunting down information across multiple sources, to stitching together data pulls, and building narratives.

Wokelo’s Agentic Workflow Builder changes that — puts an intuitive drag-and-drop canvas in your hands to design and deploy custom research agents for any use case in minutes. You can now customize and automate research, analysis, and output generation, at-scale.

What you get is a pre-trained, domain-specialized agentic workflow that:

Mirrors exactly how your team thinks, works, and delivers in a specific scenario,

Deploys on-demand and at-scale, for each instance, topic or company

Wokelo Workflows: Custom, Composable, Ready for Action

With Wokelo, you’re not confined to our library of predefined, curated workflows. Instead, you can create your own research agents — reusable, modular, and tuned to your exact process.

Unlock endless use cases meeting search and intelligence needs of every team:

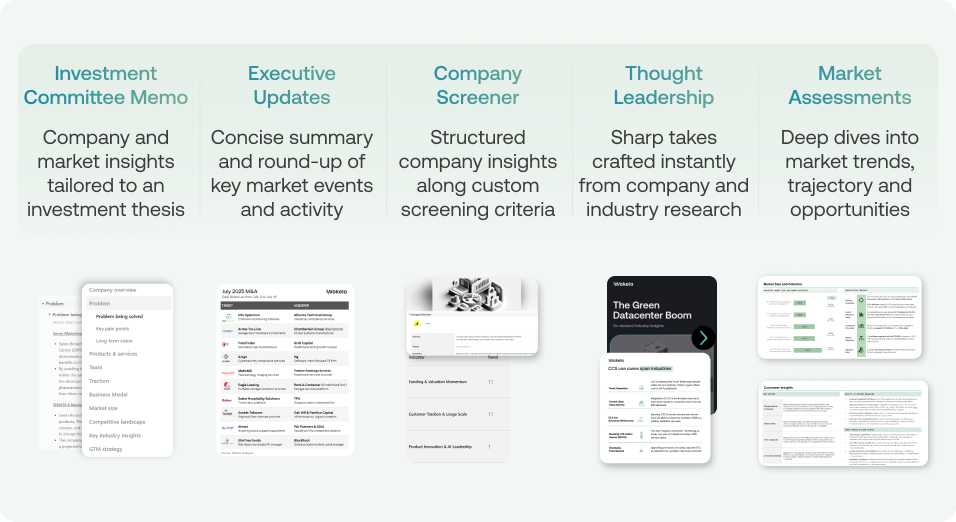

Investment Committees: Insights tailored to the investment thesis, enriched holistically with company data, industry context, and market trends.

Executive Teams / Board: Concise and timely round-up of market activity, events, or competitive moves that impact the portfolio.

Deal Management: Precise, structured insights and market maps for deal screening and evaluation, based on the organization’s screening criteria.

Marketing & Thought Leadership: Sharp, data-driven perspectives sourced from and built upon Wokelo’s research base.

Strategy and Growth: Deep dives into emerging markets, industries, and themes to explore investment and practice growth opportunities

Your research, your way

Combine the sophistication, ease, and reliability of Wokelo’s agentic AI platform, with the output type and structure that fits right into your project or deal requirements.

Whether it’s briefing for an upcoming client meeting or debriefing on portfolio performance – custom workflows extend the power of Wokelo insights and intelligence to real-world moments in your workday.

Here’s what it looks like in action:

Create Workflow Structure

Define the workflow parameters and scope, including analysis type (industry / company / fund), and user inputs and filters.

Jumpstart with Wokelo’s pre-loaded workflow templates or build from scratch for a fully custom approach.

Tailor and Enrich Analysis

Create your own analyses using custom prompts and choose from a selection of tried-and-tested models from multiple providers (OpenAI, Anthropic, Gemini, or Wokelo’s proprietary model).

Granular fine-tuning and selection for each modular analysis ensures that outputs match your team’s approach and style. Set desired output format, such as PowerPoint decks or Word documents.

Publish, Run, Share

Business users can easily preview workflow output, and test and iterate to further tailor and adapt to their user case.

Share it across your organization for consistent, repeatable insights that can be generated on-demand in just a few clicks.

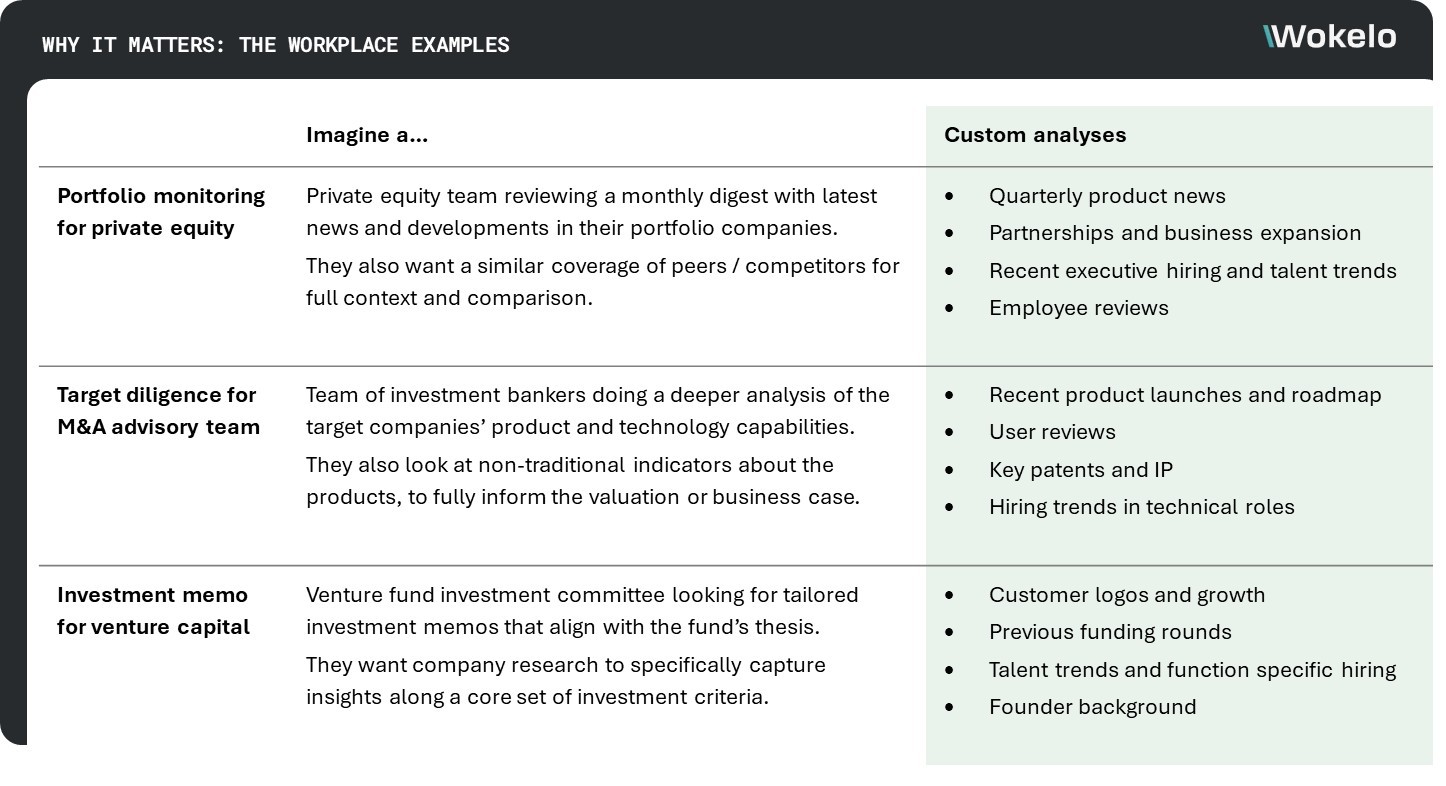

Why it Matters: The Workplace Examples

In industries like management consulting and private equity, institutionalized knowledge is a huge asset, Whether you’re dealing with fast-paced project delivery cycles or complex investment decisions, traditional manual approaches to insight gathering set you back, and the general-purpose AI and automation tools just don’t meet the intellectual rigor and bespoke demands.

The best of both worlds is where highly specialized AI capabilities can be bent and adapted to meet the use cases and problem statements of each team and stakeholder, yet in repeatable and scalable ways. Wokelo’s custom analyses serve numerous personas across investment and advisory, offering workflows that are extremely flexible as well as deterministic once tuned to your use-case.

The Agentic Workflow Builder enables business and tech teams to collaborate with full control over the research scope, AI models, and output type.

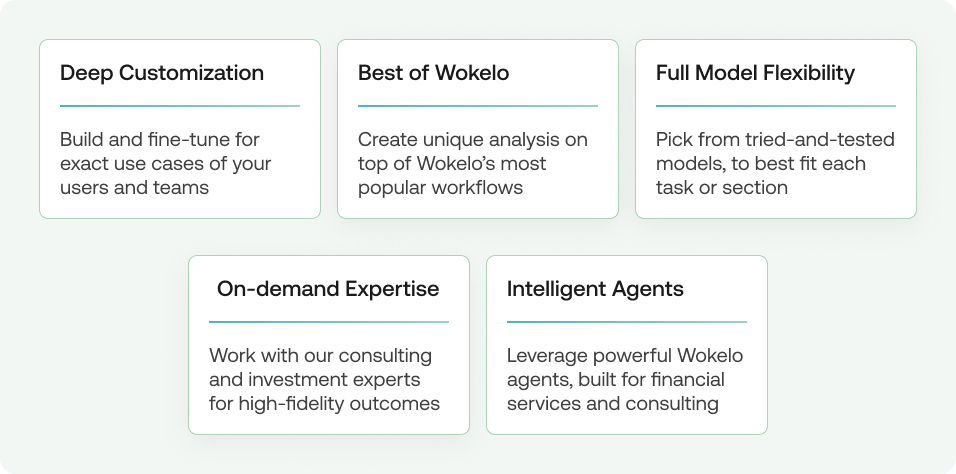

Feature Highlights & Benefits

Get the best of both worlds — granular tuning and model selection for your exact use case, and Wokelo’s existing building blocks, high-quality templates, and on-demand expertise.

Drag-and-Drop Agent Canvas:

Build and customize logic flows visually — with granular controls that enable non-technical users to easily tune workflows to their exact organization use-case.

Pre-Configured Logic Patterns

Test datasets, tweak prompts, and preview outputs before rolling out to your team. Cut down on manual QA cycles, ensuring faster iterations and higher-fidelity results.

Team-Ready Templates & Expert Consultation

Preloaded workflows for popular research scenarios, with Wokelo’s solutions team of ex-management consultants and investment bankers available to tailor builds for your needs.

Turn One-Off Tasks into Institutional IP

When research is this composable, you stop reinventing the wheel. Each custom workflow you build becomes an asset your whole organization can reuse, refine, and scale — turning ad hoc processes into institutional knowledge.

In knowledge industries where speed, accuracy, and differentiation drive advantage, Wokelo’s Agentic Workflow Builder lets you spend less time stitching together research, and more time steering the outcomes.

Investing in the Intelligent Earth: Spatial Tech is making Coordinates a Competitive Edge

Reading Time: 8minutesIn today’s data-driven economy, where decision-making windows shrink and operational stakes soar, a new class of intelligence is taking center stage: geospatial and spatial mapping solutions. Once relegated to cartographers and government agencies, these technologies are now enabling everything from autonomous driving to climate mitigation, from infrastructure modernization to AI-powered retail experiences. Recently, a flurry of high-profile venture investments, totaling over $300 million across nine deals, has spotlighted the inflection point this market is experiencing. These fundraises are clear signals in the fast-rising reliance on geospatial and spatial intelligence as a core pillar of digital transformation. This article explores the sector in-depth, spotlighting key startups developing innovative solutions and incumbents expanding the suite of offerings to serve high-value opportunties across verticals. Recent Deal Activity: Validation from Capital Markets The last eight weeks alone have seen a parade of venture capital bets across the spatial value chain: Beyond these, larger raises from ICEYE ($93M), Mapbox ($280M), and XOCEAN ($118M) in the past year further solidify investor confidence. Strategic investors like Intel Capital, Breakthrough Energy, Rio Tinto, and BHP Ventures signal long-term ecosystem participation. The Inflection Point: What’s Changed? Mapping spatial environments is not new. Governments and research institutions have used GIS […]

Reading Time: 8minutesIn today’s data-driven economy, where decision-making windows shrink and operational stakes soar, a new class of intelligence is taking center stage: geospatial and spatial mapping solutions. Once relegated to cartographers and government agencies, these technologies are …

Reading Time: 8minutes

In today’s data-driven economy, where decision-making windows shrink and operational stakes soar, a new class of intelligence is taking center stage: geospatial and spatial mapping solutions. Once relegated to cartographers and government agencies, these technologies are now enabling everything from autonomous driving to climate mitigation, from infrastructure modernization to AI-powered retail experiences.

Recently, a flurry of high-profile venture investments, totaling over $300 million across nine deals, has spotlighted the inflection point this market is experiencing. These fundraises are clear signals in the fast-rising reliance on geospatial and spatial intelligence as a core pillar of digital transformation.

This article explores the sector in-depth, spotlighting key startups developing innovative solutions and incumbents expanding the suite of offerings to serve high-value opportunties across verticals.

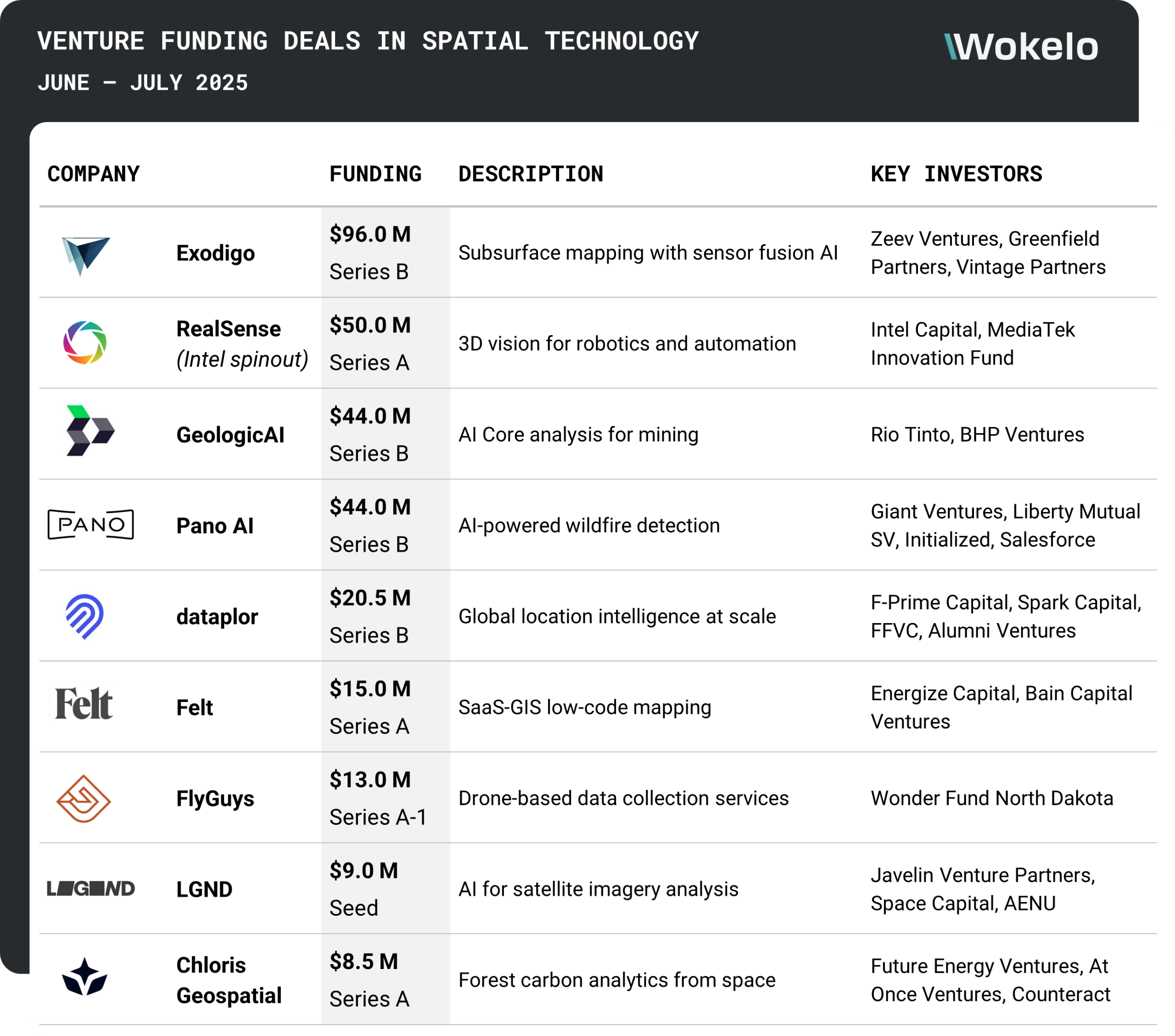

Recent Deal Activity: Validation from Capital Markets

The last eight weeks alone have seen a parade of venture capital bets across the spatial value chain:

Beyond these, larger raises from ICEYE ($93M), Mapbox ($280M), and XOCEAN ($118M) in the past year further solidify investor confidence. Strategic investors like Intel Capital, Breakthrough Energy, Rio Tinto, and BHP Ventures signal long-term ecosystem participation.

The Inflection Point: What’s Changed?

Mapping spatial environments is not new. Governments and research institutions have used GIS systems for decades. What’s changed is the velocity, accessibility, and utility of spatial intelligence, catalyzed by a powerful convergence of six interrelated forces. These drivers have transformed geospatial mapping from a specialist tool into a critical enabler of enterprise decision-making, autonomous technologies, climate response, and industrial transformation.

Advanced sensors & satellites expand the boundaries of mapping

Next-gen sensors—both orbital and terrestrial—have radically improved the resolution, frequency, and reliability of spatial data capture. Space-based platforms such as Albedo and ICEYE now offer ultra-high-resolution visible and SAR imaging, delivering near-continuous earth observation for applications from agriculture to defense.

On the ground, systems like Exodigo integrate radar, magnetic, and electromagnetic sensors to map underground infrastructure, slashing exploratory costs and improving safety. Meanwhile, drones, LiDAR, and IoT devices are collecting high-granularity spatial data in construction sites, industrial zones, and remote terrains. The spatial data supply chain is no longer static or siloed—it’s high-velocity, continuous, and multilayered, creating the foundation for more intelligent and real-time applications.

AI-powered analytics turn static maps to contextual Intelligence

The rise of GeoAI—the integration of geospatial data with AI/ML—has shifted spatial intelligence from visualization to computation. Machine learning is now applied to automate data classification, anomaly detection, and predictive modeling. City-scale projects that once took months can now be completed in a day using GPU-accelerated workflows – Esri’s mapping of Stuttgart using 200 cloud GPUs is a case in point, reducing a five-month manual process to just 24 hours.

AI-enabled image recognition, spatial embeddings, and time-series forecasting now power a growing range of applications—and transform spatial data from passive context to active decision-making input. For example, in automotive design, tools like Gravity Sketch allow designers to model 3D environments that interact with vehicle simulations.

Cloud-first architecture lowers adoption and integration barriers

Legacy GIS deployments were CapEx-intensive, often requiring six-figure investments and long lead times. The modern spatial stack is different, with platforms like Felt, LGND, and RealSense removing the infrastructure and cost burdens that once limited geospatial adoption.

This SaaS-driven model also enables seamless integration with business tools—embedding geospatial workflows into enterprise dashboards, mobile apps, and field operations. As a result, spatial functionality is no longer siloed within specialized GIS teams; it’s available at the edge, to decision-makers across industries. Moreover, cloud platforms now offer native spatial query capabilities (e.g., Redshift + CARTO), allowing geospatial workflows to be embedded directly into analytics dashboards, enterprise apps, or even mobile UIs.

Cross-sector applicability means value delivery at scale

What truly distinguishes this moment is the sectoral breadth of adoption. Once limited to government agencies, spatial intelligence is now fueling innovation across:

Automotive: HERE Technologies’ HD Live Maps deliver centimeter-level accuracy for NIO’s vehicles, supporting intelligent lane positioning and autonomous driving features.

Agriculture & Mining: GeologicAI’s scanning platforms support mineral exploration, while Agri-GIS apps in India are helping over 150,000 farmers boost yields using geospatial recommendations.

Public Safety & Climate Tech: Pano AI enables wildfire detection via panoramic camera networks, while Chloris Geospatial helps companies measure carbon stocks and nature-based offsets from space.

Retail & Logistics: Augmodo’s in-store digital twins and navigation platforms offer real-time inventory insights. Spatial intelligence is also enabling advanced fleet management, dynamic pricing, and hyperlocal marketing.

In fact, 74% of enterprise data buyers now use location intelligence, and 97% of large companies have spatial analytics embedded into their planning and operations.

Autonomous systems and the need for real-time spatial awareness

As vehicles, robots, and drones become more autonomous, their need for continuous, high-fidelity spatial awareness becomes existential.

Spatial intelligence now combines 3D mapping with AI to create dynamic, responsive environments for machines. From real-time obstacle detection to pathfinding through complex terrains, the tech stack enables autonomous systems to not just navigate—but to make decisions based on their surroundings.

Key enablers here include:

Sensor fusion (e.g., camera + LiDAR + radar)

Real-time edge processing via GPUs

Streaming data integrations from IoT sensors

Digital twins and simulation platforms that train and test systems in virtualized spatial environments

This sector alone is forecasted to help push the spatial computing market from $135B in 2024 to $1.06T by 2034, with autonomous vehicles and drones as prime growth engines.

The rise of synthetic data and simulations for scenario planning

Another subtle but powerful inflection point is the role of synthetic data in improving spatial solutions. Synthetic imagery, derived from simulation or generative models, is being used to fill gaps in geospatial datasets—especially in high-risk, low-visibility environments (e.g., war zones, deep sea, underground).

By combining real and synthetic data, platforms can simulate urban flooding, map unknown terrain, or model climate impacts on infrastructure. This supports not just predictive analytics, but scenario planning—critical for resilience and risk mitigation.

Synthetic datasets also help train AI models in data-poor geographies or edge use-cases, accelerating product readiness and reducing data acquisition costs.

The Market Opportunity: A Trillion-Dollar TAM Taking Shape

Industry estimates vary, but all point steeply upward, with geospatial analytics exceeding $230 billion in market size by 2023. The adjacent spatial computing market is projected to touch a trillion dollars by 2034, growing at a substantial CAGR of 22.6%. The market is being driven by surging demand from multiple adjacent industries.

In transportation and infrastructure, adoption is rising rapidly—spatial data usage in logistics and smart-city systems is enabling dynamic routing, predictive maintenance, and resilient planning. In insurance, utilities, and energy, spatial tools are critical for risk pricing, asset monitoring, and climate resilience. Sectors such as construction and mining increasingly rely on spatial intelligence to reduce overruns, as nearly all large projects face delays due to geological uncertainty and data gaps.

Meanwhile, retail and consumer-focused industries are embedding spatial mapping for in-store navigation, personalized location-based services, and inventory efficiency. At the same time, public sector and ESG mandates are accelerating investment. Governments entities across emerging and developed markets, such as India and UAE, are deploying digital twin mapping to track emissions, sea-level shifts, and climate infrastructure.

Ultimately, the convergence of AI enabled GeoAI, edge-connected sensors (LiDAR, IoT, satellite), and cloud-native delivery is enabling spatial intelligence to scale across verticals. Sectors ranging from logistics and urban planning to insurance and retail are evolving into natural adopters—transforming spatial mapping from niche to mainstream, and continuing to feed consistent adoption well into the next decade.

Value Chain Decomposition: Mapping the Investment Landscape

Understanding where value accrues is key. The spatial intelligence value chain consists of four primary layers:

Data Acquisition: Companies like Planet Labs, ICEYE, Exodigo, and FlyGuys focus on generating new datasets. Advances in LiDAR, thermal, SAR, and multi-spectral imaging are enhancing frequency, resolution, and cost-efficiency.

Processing & Orchestration: LGND, CARTO, and Esri operate at the layer of analytics, workflow orchestration, and visualization. This is where differentiation via AI and ML comes into play. RealSense and Trimble add hardware-software fusion to deliver end-to-end insights.

Application & Integration: Tech Mahindra’s Altavec, Samsara-Esri integrations, and Autodesk Forma represent the connective tissue integrating geospatial insights into enterprise workflows—from fleet management to urban design.

User Interfaces: ARway, Augmodo, and Apple Vision Pro are translating spatial intelligence into interactive, monetizable front-end experiences, particularly in retail, travel, and built environments.

Each layer offers different margin profiles, defensibility, and integration complexity. Investors should evaluate which layer a startup plays in—and whether it controls or commoditizes adjacent layers.

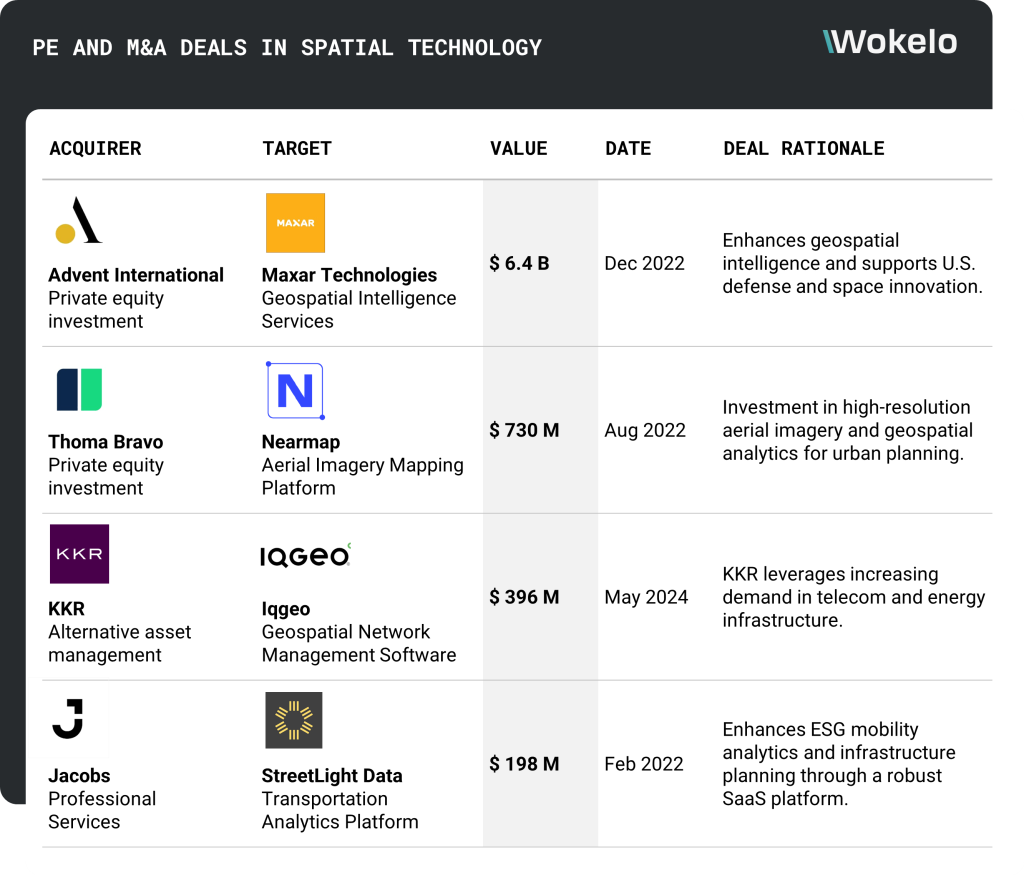

Exit Outlook: Consolidation, IPOs, and Strategic Appetite

IPO activity is already gaining momentum. Synspective, a Japan-based developer of small SAR (synthetic aperture radar) satellites for disaster response and infrastructure monitoring, went public in December 2024 at a $370 million valuation. In May 2024, NextGeo, an Italian marine geoscience firm specializing in offshore surveys for energy infrastructure, also listed publicly.

In the last 2 years, Private Equity investors have also been picking up a share of the evolving market, complementing their core asset portfolios with intelligence layers.

As spatial tooling specialists and end-industries realize the value from consolidation and deep integration, a continued streak of M&A activity, strategic investment, and partnerships by incumbents is on the horizon:

Autodesk

Autodesk acquired Forma for AI-assisted urban design and invested in VAPAR and GAMMA AR to enhance infrastructure inspection and AR-based BIM overlays.

These moves deepen Autodesk’s spatial modeling, environmental simulation, and real-time site collaboration capabilities, aligning with its broader push into digital twins and cloud-native infrastructure planning.

Trimble

Trimble’s acquisition of Cityworks added GIS-integrated asset management for public infrastructure, while Bilberry brought AI-driven precision agriculture.

Together, they expand Trimble’s presence in smart cities and farming by combining geospatial data with operational automation, reinforcing its location intelligence and industry-specific analytics plays.

Esri

Esri enhanced ArcGIS by acquiring Zibumi (3D simulation), indoo.rs (indoor mapping), and nFrames (photogrammetry).

These acquisitions deepen Esri’s ability to offer immersive 3D models, real-time indoor navigation, and high-resolution digital twins — extending its geospatial leadership from outdoor maps into detailed, dynamic spatial environments.

Ford

Ford acquired Geotab to bolster its connected vehicle and fleet intelligence platform.

Geotab’s expertise in real-time spatial analytics, route optimization, and predictive maintenance enhances Ford’s commercial fleet offerings, supporting its broader strategy around smart mobility, EV adoption, and telematics-enabled logistics.

GM Ventures

GM Ventures has backed companies like GeoDigital, a leader in LiDAR-based 3D mapping, and Xevo, known for connected vehicle data platforms.

These investments help GM embed high-definition maps, spatial context, and predictive intelligence into its autonomous and connected vehicle systems.

Toyota

Toyota has partnered with firms such as HERE Technologies, Mapbox, and TomTom to integrate high-precision spatial mapping into its ADAS and autonomous vehicle platforms.

These alliances enhance real-time navigation, HD localization, and environmental awareness—core to Toyota’s efforts in autonomy, safety, and intelligent vehicle systems.

Expect enterprise software giants, industrial players, and large public sector IT providers to enter acquisition mode as spatial capabilities become table stakes.

Key Investor Filters: What to Look for in a Spatial Bet

To separate hype from durability, investors should probe:

Time-to-Insight Efficiency: Can the platform deliver real-time analytics at scale? Look for GPU-native backends, cloud integrations, and high-throughput data pipelines.

End-User Usability: Do various enterprise users have access to these insights? Democratization is a revenue catalyst. Solutions like Felt and ARway demonstrate how low-code/no-code interfaces expand adoption.

Go-to-Market Leverage: Is the product embedded in critical workflows (e.g., Autodesk, Esri integrations)? Channel partnerships reduce CAC and expand reach.

Sector Focus vs. Platform Optionality: While vertical SaaS (e.g., GeologicAI) has depth, platforms like LGND or CARTO have horizontal optionality. Both models can work—just assess execution risk accordingly.

Regulatory Alignment: Built-in privacy, encryption, and compliance features matter, especially in healthcare, defense, and law enforcement deployments.

Final Takeaway: The Democratized Era of Spatial Tech

The story of spatial mapping is not just about maps or satellites. What was once a set of static visual imagery has now become a living, learning, decision-support layer embedded across verticals, devices, and institutions. This sector sits at the intersection of autonomy, sustainability, digitization, and immersive experiences.

No longer just describing the environment but orchestrating it, these technologies are seeing high ROI use cases, supportive regulation, accelerating cloud economics, and clear enterprise buy-in. What’s emerging is the next foundational infrastructure and data layer —much like cloud or mobile did in previous decades.

For investors, the window is still open. The winners of tomorrow’s spatial stack are being formed—and funded—today.

Disclosure: This post draws from the latest research and transaction data generated by Wokelo AI Platform as of July 2025. No forward-looking investment recommendations are offered.

From Billable Hours to AI Agents: Investors are Rushing in to Scale Legal Tech

Reading Time: 6minutesIn just the past week alone, five venture capital deals have illuminated the breadth and depth of innovation within legal tech, with startups like Callidus Legal AI, Covenant, and Tavrn raising capital from top-tier firms such as Cervin Ventures, Flybridge Capital, and Left Lane Capital. These deals represent a surge of investor confidence in an industry reshaping every use case from litigation and compliance to contract automation and public policy analysis. But let’s break down the attractiveness of the AI and automation opportunity in even simpler terms. Here’s an industry characterized by massive volumes of unstructured knowledge mining and manual paperwork, perhaps more than any other sector in the modern world. Enter any law office in the movies or real life – the floor-to-ceiling shelves of legal volumes and files is a persistent background, and analyzing 400-page long document stacks without a blind spot is the daily expectation of any professional. For investors seeking high-growth opportunities underpinned by structural inefficiencies ripe for AI disruption, legal tech is now impossible to ignore. Let’s dive into how a nexus of AI innovation, cloud transformation, and regulatory evolution is shaping investment opportunities in the centuries-old profession. Legal Tech Market Trends Not to be […]

Reading Time: 6minutesIn just the past week alone, five venture capital deals have illuminated the breadth and depth of innovation within legal tech, with startups like Callidus Legal AI, Covenant, and Tavrn raising capital from top-tier firms such …

Reading Time: 6minutes

In just the past week alone, five venture capital deals have illuminated the breadth and depth of innovation within legal tech, with startups like Callidus Legal AI, Covenant, and Tavrn raising capital from top-tier firms such as Cervin Ventures, Flybridge Capital, and Left Lane Capital. These deals represent a surge of investor confidence in an industry reshaping every use case from litigation and compliance to contract automation and public policy analysis.

But let’s break down the attractiveness of the AI and automation opportunity in even simpler terms. Here’s an industry characterized by massive volumes of unstructured knowledge mining and manual paperwork, perhaps more than any other sector in the modern world. Enter any law office in the movies or real life – the floor-to-ceiling shelves of legal volumes and files is a persistent background, and analyzing 400-page long document stacks without a blind spot is the daily expectation of any professional.

For investors seeking high-growth opportunities underpinned by structural inefficiencies ripe for AI disruption, legal tech is now impossible to ignore. Let’s dive into how a nexus of AI innovation, cloud transformation, and regulatory evolution is shaping investment opportunities in the centuries-old profession.

Legal Tech Market Trends Not to be Missed

Signal-Rich Deal Activity is Here to Stay

The venture activity from last week captured an evolving interest across multiple segments of legal tech:

Tavrn secured $15M to automate pre-litigation workflows for personal injury law, combining generative AI with domain-specific document creation.

Callidus Legal AI brought in $10M to power litigation drafting, surfacing legal arguments, and automating brief generation with large-scale precedent analysis.

Covenant raised $4M to offer AI-driven tools for private equity legal reviews, bringing tailored solutions to institutional investors navigating complex fund agreements.

Helios raised $4M to streamline government affairs and public policy compliance with AI tools that monitor legislation and track regulatory shifts.

Chariot Claims closed $3.6M to simplify class-action participation for consumers, democratizing access to legal recourse.

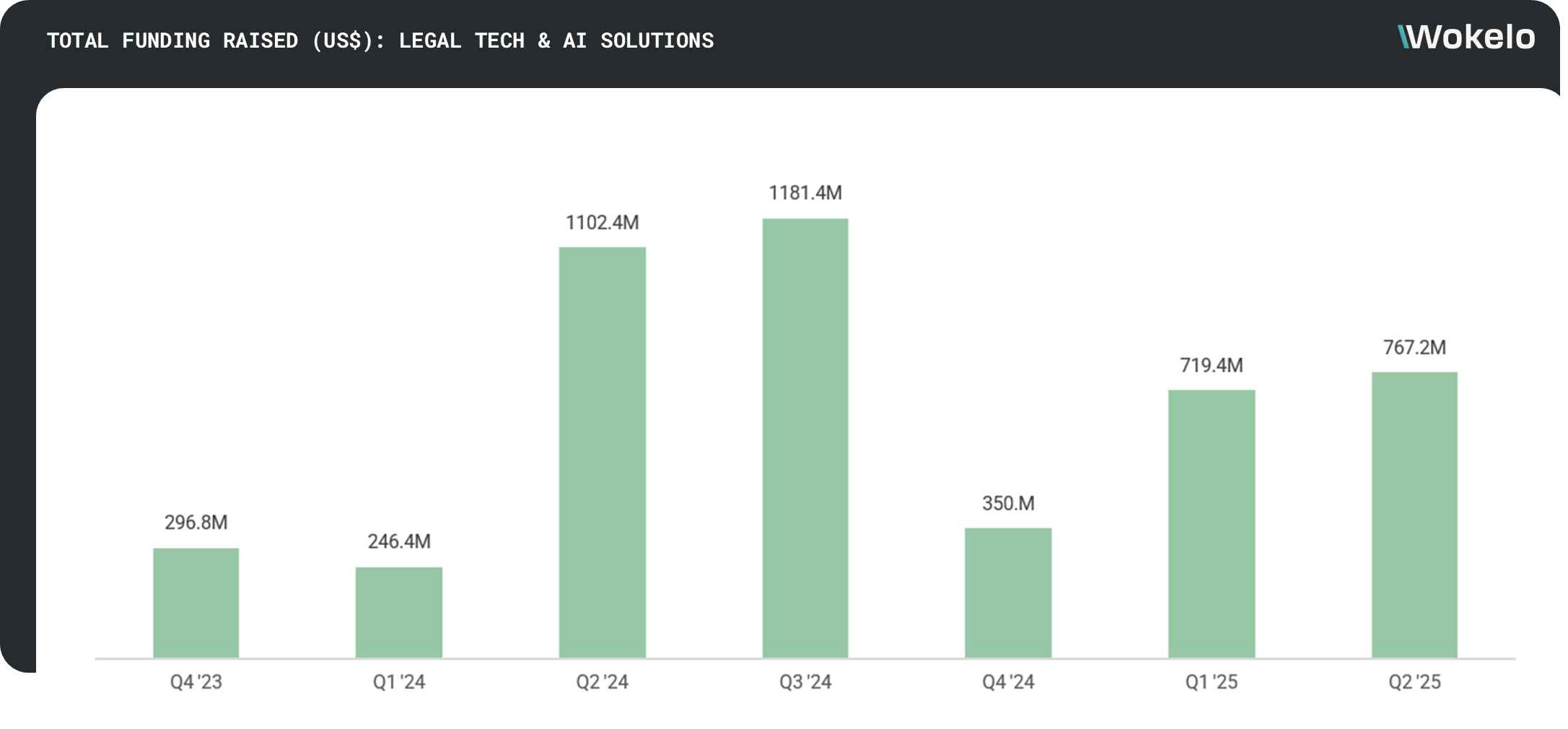

These startups span the legal tech value chain, from consumer-facing claim processing to institutional-grade investment contract analysis. And this certainly wasn’t an isolated phase of interest – Our analysis of the legal tech market over the past couple of years shows a fluctuating yet persistant dealmaking landscape even amidst a broader dampening of VC.

Collectively, this market actvity signals that tech and AI-driven automation is not just augmenting traditional law offices, it is rearchitecting processes and operations towards a digital-native future that’s drawing even the likes of Google and Amazon into the investment fold.

Market Size and Investor Appetite: More Than a Niche

Legal tech is a $29.6B industry today, projected to more than double by 2034. The AI-powered legal segment alone is growing at 36% annually. In 2024, despite a broader tech slowdown, legal tech startups raised near $3B in funding, and are showing promising signs of steady growth in the recent quarters.

Landmark deals showcase how prominent investors are placing long-term bets:

Clio raised $900M to deepen its global platform and expand into AI-powered research via its $1B acquisition of vLex.

Harvey raised $300M from Coatue and Kleiner Perkins to scale legal agentic AI, expanding beyond law into tax and compliance.

Norm AI and Supio attracted capital from top firms including Bain, Sapphire Ventures, and Blackstone Innovations.

The financing scale, investor quality, and company traction demonstrate that legal tech has moved way beyond an early-stage play to an infrastructure build-out.

Enterprise Adoption: Law Firms, Corporates, and Governments on Board

Institutional validation is pouring in from multiple angles, with the incumbents and upstarts coming together in a thriving ecosystem:

Thomson Reuters acquired Casetext for $650M to embed generative AI into its legal research platform.

Wolters Kluwer bought Brightflag for $479M to bolster its AI-powered legal spend analytics.

Morgan Lewis and LexisNexis are partnering with AI startups to co-develop new legal products.

According to the 2024 American Bar Association’s Legal Technology Survey Report, AI usage among law firms has increased from 11% in 2023 to 30% in 2024. Larger firms with more than 100 attorneys have higher AI adoption rates at 46%, while mid-sized firms (10-49 attorneys) are at 30% and solo practitioners at 18%.

And no, the market is not hinging on the a futuristic view of a virtual courtroom staffed by AI agents for lawyers and jurors. There are plenty of real-world problem statements and use cases to solve for – rife with grunt work, drab office days, bottlenecks and delays, and perpetual fear of blind spots or missed insights. For example, 35% of respondents use AI for legal research, making it the primary application of AI in legal tech.

Studies estimate that up to 44% of legal work could potentially be automated, enhancing operational efficiency. U.S. lawyers could gain 266 million hours of productivity annually by automating routine tasks. These aren’t just theoretical estimates, with companies seeing impressive adoption and outcomes that will underpin rapid scaling of AI tools across the legal profession:

Robin AI reduced contract review time by 85%, freeing up senior lawyer bandwidth.

Gavel’s AI assistant for small firms saw adoption in under 20 minutes of trial.

Avantia reported a 48% margin uplift from shifting NDA work to AI-powered processes.

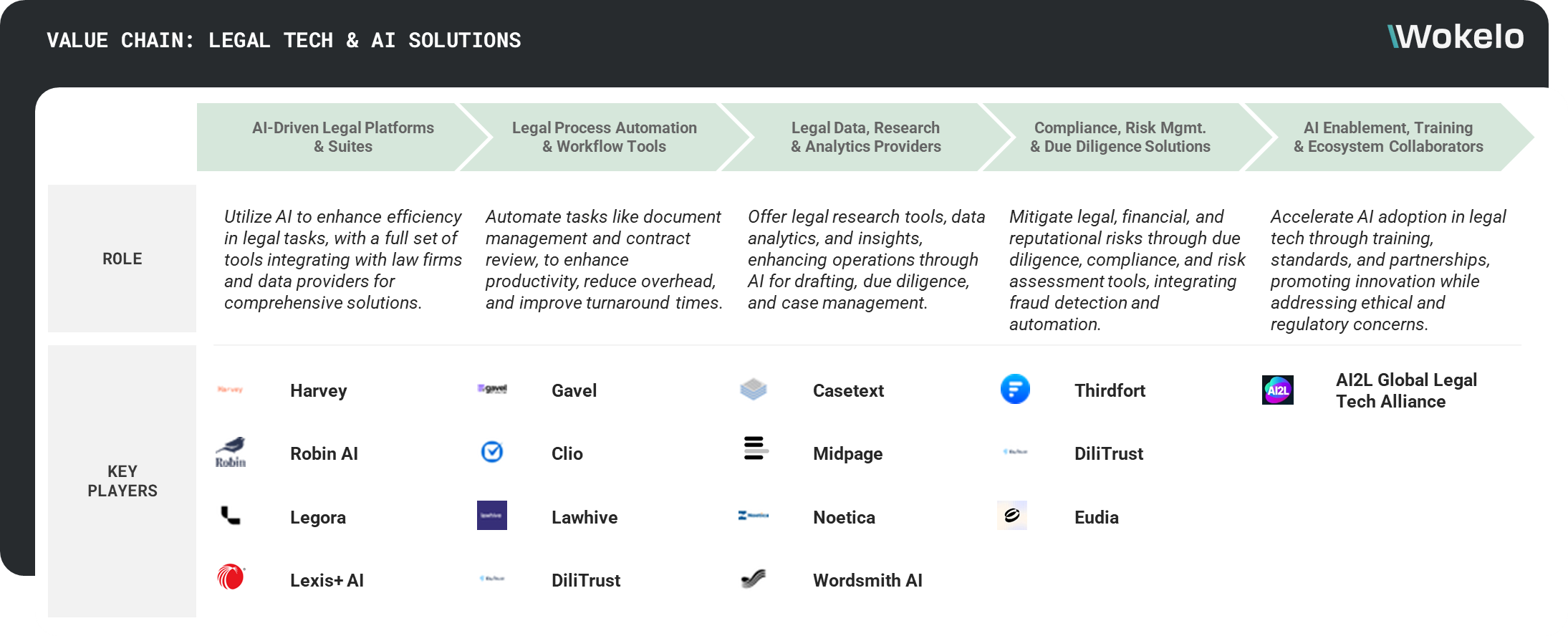

What AI Is Disrupting: High-Leverage Use Cases in Legal

Investors should focus on areas where AI addresses high-value legal pain points, such as resolving deeply-engrained inefficiencies, democratizing access to legal recourse and solutions, and enhancing proactive compliance.

Contract Lifecycle Management (CLM): Platforms like Legora and Ironclad use generative AI to draft, redline, and review contracts with accuracy and speed.

Litigation Drafting & Legal Research: CallidusAI and Casetext offer systems that generate full motion drafts, leveraging retrieval-augmented generation (RAG) to surface relevant precedent.

Public Policy and Compliance: Helios’ Proxi tool tracks regulations in real time, aiding legal and government affairs teams in monitoring legislation and drafting policy briefs.

Claims Automation & Consumer Justice: Chariot Claims and EvenUp are using AI to expand access to justice by simplifying claims filing and pre-litigation document generation.

Private Market Legal Infrastructure: Covenant targets fund investors with AI markups for NDAs and LPAs, delivering institutional-grade legal insights at startup speed.

Business Model Evolution: Monetizing Intelligence, Not Hours

The legacy law firm model of billing hours is incompatible with AI-driven productivity. Legal tech startups are adopting:

Usage-based pricing (e.g., Tavrn)

Flat annual fees with task-based add-ons

SaaS subscriptions with collaborative document ecosystems (e.g., Legora, Gavel)

This shift is critical: it aligns incentives with value creation, not time spent. It also creates defensible recurring revenue models attractive to institutional investors.

Regulatory Tailwinds and Governance Maturity

Legal tech isn’t scaling in a vacuum. As one of the trickiest industries to apply technoology and automation to, meeting regulatory, governnce and ethical standards is of utmost importance. The good news is that the industry bodies and legislative authorities responsible for this aspect are catching up fast – both in terms of enabling adoption and governing it:

The Puerto Rico Supreme Court has mandated technology competence for lawyers, understanding the benefits, limitations, and risks of emerging technologies. This aligns with trends in regions such as England, Australia, Arizona, and the District of Columbia

The American Bar Association‘s Formal Opinion 512 emphasizes that legal professionals must perform due diligence, reviewing data security and confidentiality measures employed by legal tech vendors, including compliance with standards like SOCII and HIPAA.

What’s Next for Investors to Look Out for in Legal Tech

The legal tech revolution isn’t about replacing lawyers—it’s about reengineering legal infrastructure with the same user-centric and scalable models that fintech applied to banking. As AI, cloud, and compliance converge, capital and innovation are coalescing around five core opportunity zones that are reshaping how legal work is delivered, consumed, and monetized:

1. Vertical Infrastructure Layers for Specialized Legal Domains We’re seeing a rise in purpose-built legal platforms tailored to complex, high-value workflows like private fund diligence and regulatory compliance. These go beyond generic contract tools, with sector-native operating systems that integrate legal logic, compliance rules, and AI-native automation. Covenant and Norm AI exemplify this trend of embedding intelligence into the critical infrastructure of institutional investing and enterprise governance.

2. High-Fidelity Legal Research and Drafting Tools As large language models evolve, legal tech players are racing to build differentiated layers using proprietary datasets and retrieval-augmented generation (RAG). This enables more precise outputs, better citations, and faster document generation—essential for litigation-heavy domains. Callidus, Midpage, and Legora are innovating here with tools that collapse week-long drafting tasks into minutes, unlocking productivity without compromising legal rigor.

3. Platform Consolidation and Ecosystem Playbooks The emergence of end-to-end legal operating systems mirrors what Salesforce did for CRM. Harvey and Clio are leading the charge by acquiring and integrating complementary tools, from research engines to client intake to billing. Investors should expect more M&A as platforms compete to become the system of record for legal workflows across firms, departments, and geographies.

4. Global and Down-Market Expansion for Access and Affordability Legal services are notoriously inaccessible in emerging markets and for underserved small businesses. New entrants are flipping the economics by deploying AI-driven self-service tools at scale. Jusbrasil in Latin America and Lawhive in the UK are reshaping access models, enabling “main street law” to operate with enterprise-grade tooling at consumer-grade pricing. This is a powerful wedge for global expansion.

5. Compliance, Risk, and the Expansion into Enterprise Ops Legal tech is extending beyond courts and contracts into areas like ESG reporting, fraud detection, and regulatory intelligence. As the compliance burden grows and legislation shifts rapidly, enterprises are demanding real-time, explainable, and auditable solutions. Norm AI, Thirdfort, and EQS are building platforms that integrate directly into risk, finance, and operations, opening a far larger TAM than traditional legal practice.

These themes aren’t isolated—they’re converging. The next breakout companies will likely sit at the intersection of multiple vectors: vertically specialized, AI-native, globally scalable, and seamlessly integrated into broader enterprise stacks.

Disclosure: This post draws from the latest research and transaction data generated by Wokelo AI Platform as of July 2025. No forward-looking investment recommendations are offered.

How Seven Two Partners Unlocked Hidden Portfolio Insights with Wokelo, Securing a $50B FoF Client Renewal

Reading Time: 3minutesFor boutique advisory Seven Two Partners, delivering unparalleled value to its leading Fund-of-Funds (FoF) clients means navigating a deluge of complex information—often involving individual fund files exceeding 100 documents and 50+ pages each. Facing the daunting task of monitoring over 1000 underlying portfolio holdings and mountains of such fund documentation, their lean team risked missing critical insights. Wokelo enabled them to unearth intelligence on portfolio companies that even their $50B AUM FoF client was unaware of, cementing their role as an indispensable partner and compressing their exhaustive fund diligence from 20 days to just one week. The Transformation, by the Numbers: The Stakes: Boutique Excellence in a Data-Saturated World Client Profile: Seven Two Partners is a boutique investment firm renowned for its bespoke advisory services to leading Funds-of-Funds. With a lean, expert team, they pride themselves on a proprietary diligence methodology that’s honed over decades, providing deep insights and strategic counsel to sophisticated institutional investors. The Challenge: Drowning in Data, Striving for Alpha For Seven Two Partners, maintaining an edge and delivering exceptional value was becoming increasingly difficult: The Wokelo Solution: AI-Powered Diligence & Monitoring Seven Two Partners partnered with Wokelo AI to implement a multi-faceted solution that augmented their […]

Reading Time: 3minutesFor boutique advisory Seven Two Partners, delivering unparalleled value to its leading Fund-of-Funds (FoF) clients means navigating a deluge of complex information—often involving individual fund files exceeding 100 documents and 50+ pages each. Facing the daunting …

Reading Time: 3minutes

For boutique advisory Seven Two Partners, delivering unparalleled value to its leading Fund-of-Funds (FoF) clients means navigating a deluge of complex information—often involving individual fund files exceeding 100 documents and 50+ pages each. Facing the daunting task of monitoring over 1000 underlying portfolio holdings and mountains of such fund documentation, their lean team risked missing critical insights.

Wokelo enabled them to unearth intelligence on portfolio companies that even their $50B AUM FoF client was unaware of, cementing their role as an indispensable partner and compressing their exhaustive fund diligence from 20 days to just one week.

The Transformation, by the Numbers:

Fund diligence time compressed to under a week (vs 20 days), a 70% reduction

Secured advisory with a $50B AUM FoF by delivering unique portco insights

The Stakes: Boutique Excellence in a Data-Saturated World

Client Profile: Seven Two Partners is a boutique investment firm renowned for its bespoke advisory services to leading Funds-of-Funds. With a lean, expert team, they pride themselves on a proprietary diligence methodology that’s honed over decades, providing deep insights and strategic counsel to sophisticated institutional investors.

The Challenge: Drowning in Data, Striving for Alpha

For Seven Two Partners, maintaining an edge and delivering exceptional value was becoming increasingly difficult:

Overwhelming Fund Diligence: Each fund diligence process was notoriously complex and lengthy, involving the manual review of over 100 individual files, many exceeding 50 pages each—a “nightmare” to process thoroughly.

Risk of Missed Critical Information: The sheer volume—thousands of pages per fund—made it nearly impossible to catch every nuance, red flag, or hidden opportunity within fund documentation.

Massive Portfolio Monitoring Task: Staying abreast of developments across more than 1000 underlying portfolio company holdings for their FoF clients was a monumental undertaking for the lean team.

Pressure to Add Demonstrable Value: FoF clients expected Seven Two Partners to be on top of industry trends and, crucially, what was happening within their extensive underlying portfolios, a task complicated by the sheer scale of data.

Ineffective Legacy Tools: Reliance on generic solutions like Google News for monitoring the 1000+ holdings resulted in too much noise, redundant information, and a lack of relevance.

The Wokelo Solution: AI-Powered Diligence & Monitoring

Seven Two Partners partnered with Wokelo AI to implement a multi-faceted solution that augmented their expertise and streamlined their core processes by handling vast information:

Custom-Built Fund Diligence AI: Wokelo implemented a bespoke fund diligence template mirroring Seven Two Partners’ proprietary methodology. This AI-powered system was designed to efficiently process the hundreds of voluminous files per fund, effectively digitizing and accelerating their decades of investment experience.

Targeted Fund & Portfolio Company Monitoring: Wokelo set up multiple, highly specific weekly newsfeeds to track crucial developments across the 1000+ underlying portfolio holdings, filtering out noise and delivering relevant intelligence directly.

Comprehensive Company Diligence: The platform provided tools for deeper dives into specific companies as needed, supporting both the detailed fund diligence and ongoing monitoring of the extensive portfolios.

Team Empowerment & Customization: Wokelo’s team trained Seven Two Partners’ internal staff to configure the platform, customize templates for various diligence scenarios, and adapt the AI to their evolving use-cases directly within the platform.

Strategic Impact: From Data Overload to Decisive Insights

The integration of Wokelo AI delivered transformative results, enabling Seven Two Partners to elevate its service and strategic position:

Secured & Enhanced Key Client Relationship: The most striking impact came when Wokelo AI helped Seven Two Partners provide critical insights on portfolio companies that their client—a leading FoF/PE player with $50B in AUM—was not even aware of. This demonstration of being deeply informed, despite the 1000+ holdings to track, was instrumental in renewing a vital advisory service agreement.

Radically Accelerated Fund Diligence: The time required for comprehensive fund diligence, typically involving those 100+ extensive files, was slashed from 20 days to just one week—an over 70% reduction, making the process more than 3x faster and allowing the team to increase throughput.

Proactive Risk & Red Flag Identification: Wokelo AI’s ability to systematically process vast amounts of information from lengthy documents enabled Seven Two Partners to uncover potential risks and red flags within funds much earlier than previously possible with limited human bandwidth.

Enabled Scalable Advisory Practice: By automating and streamlining the laborious research and monitoring of thousands of data points across funds and companies, Wokelo AI empowered Seven Two Partners to effectively grow their business, taking on more clients with the same team size.

Elevated Value Proposition: The ability to consistently deliver unique, data-driven insights on funds and their 1000+ underlying holdings significantly enhanced Seven Two Partners’ reputation and value to their sophisticated FoF clientele.

For Seven Two Partners, Wokelo AI provided the critical leverage to transcend the limitations of a lean team structure when faced with institutional-scale data. By marrying their deep industry expertise with Wokelo’s AI-powered intelligence to manage hundreds of documents and over a thousand portfolio companies, they not only solved their scaling challenges but also unlocked new levels of client value and competitive differentiation.

Is Your Firm Ready to Unlock its Full Investment Potential?

Discover how Wokelo AI can transform your deal flow, empower your team, and accelerate your path to high-conviction investments.

Power-Hungry Big Tech is Boarding Every Nuclear Energy Train to The Future

Reading Time: 4minutesA decade ago, few investment committees would have predicted that nuclear power, the pariah of the clean energy revolution, would command the rapt attention of Silicon Valley, Wall Street, and Washington. Yet, as 2025 unfolds, nuclear is not just back. It is being reborn, with the world’s largest technology companies at the front of the charge and a stream of capital, M&A deals, and legislative reforms creating a moment of historic significance for long-term institutional investors. What we are witnessing is not simply a sector pivot, but the resurgence of nuclear energy as the very foundation for the next era of digital infrastructure. This wave of nuclear investments and broader nuclear energy investments is underpinned by irrefutable numbers, decisive strategic bets from technology and industrial giants, and a new political consensus that nuclear is indispensable for climate resilience and energy security. Why Nuclear? Why Now? Geopolitics & Climate Collude in an Appeal of Nuclear Baseload Investors were already hungry for non-fossil “baseload” energy when Russia’s invasion of Ukraine threw commodity markets into chaos. As nations scrambled to secure domestic energy supplies, nuclear power’s promises of ultra-high-capacity factors (>90%), minimal emissions, and energy security became impossible to ignore. Nations like the […]

Reading Time: 4minutesA decade ago, few investment committees would have predicted that nuclear power, the pariah of the clean energy revolution, would command the rapt attention of Silicon Valley, Wall Street, and Washington. Yet, as 2025 unfolds, nuclear …

Reading Time: 4minutes

A decade ago, few investment committees would have predicted that nuclear power, the pariah of the clean energy revolution, would command the rapt attention of Silicon Valley, Wall Street, and Washington. Yet, as 2025 unfolds, nuclear is not just back. It is being reborn, with the world’s largest technology companies at the front of the charge and a stream of capital, M&A deals, and legislative reforms creating a moment of historic significance for long-term institutional investors.

What we are witnessing is not simply a sector pivot, but the resurgence of nuclear energy as the very foundation for the next era of digital infrastructure. This wave of nuclear investments and broader nuclear energy investments is underpinned by irrefutable numbers, decisive strategic bets from technology and industrial giants, and a new political consensus that nuclear is indispensable for climate resilience and energy security.

Why Nuclear? Why Now?

Geopolitics & Climate Collude in an Appeal of Nuclear Baseload

Investors were already hungry for non-fossil “baseload” energy when Russia’s invasion of Ukraine threw commodity markets into chaos. As nations scrambled to secure domestic energy supplies, nuclear power’s promises of ultra-high-capacity factors (>90%), minimal emissions, and energy security became impossible to ignore.

Nations like the United States, France, China, and India are scaling up nuclear at an unprecedented pace, with operational reactor capacity set to surge from 413 GW (2022) to an estimated 812 GW by 2050—driven by annual additions reaching 27 GW in the 2030s. These nuclear energy investments are unlocking a new era of dependable baseload capacity, driving a global reallocation of capital into climate-friendly assets.

A Once-in-a-Generation Capital Cycle

Annual global investments are projected to leap past $100 billion by 2030 (up from $30 billion in the 2010s), and advanced nuclear energy’s cumulative capex is measured in the hundreds of billions through 2050. Government reforms, such as the US ADVANCE Act and Nuclear Permitting Reform Bill, are defusing capital risk by streamlining permitting and pushing loan guarantees and tax credits into the sector, accelerating new nuclear investments.

It’s no wonder, then, that nuclear energy stocks have hit record growth rates in the last few months. But this cycle is remarkable for another reason: it is being driven as much by the energy needs of the digital economy as by legacy utilities.

Big Tech Pivot: Google, Microsoft, Amazon Go Nuclear

From Hype to Hardware – Data Centers and AI as Market Catalysts

The most critical signal for investors is the bold entry of big tech as anchor offtakers, direct investors, and strategic partners in nuclear energy. The voracious power appetite of AI and hyperscale data centers means computing and storage cannot be left at the mercy of intermittency; only nuclear can deliver the “always-on,” carbon-free gigawatts that tech giants require. The rise of AI data centre energy demand is accelerating this transformation across global infrastructure.

Recent Landmarks:

Google: Capital to Elementl Power for three advanced nuclear projects (~600 MW each) with a >10 GW target by 2035

Amazon: Over $1 billion in nuclear projects; $500M stake in X-energy’s Xe-100 SMR to power AWS

Microsoft: Multiple nuclear PPAs and investments in modular reactor startups

Meta: With global consortiums pledging to triple nuclear capacity by 2050

These are not token gestures but multi-year, multi-gigawatt infrastructure bets. Just a subset of AI-driven data center demand in the U.S. could justify hundreds of new nuclear reactors. This shift signals a deeper trend of AI energy investment, particularly within nuclear powered data center initiatives.

Technology as Value Differentiator

As with all their other bets, the tech giants are not just investing, but shaping the nuclear technology stack. Google’s backing of advanced reactor firm Kairos, and Amazon’s hand in modular reactor deployment, reflects an appetite for solutions that collapse cost, time, and scale barriers while radically improving safety. Their commitments reflect the strategic value of Big Tech’s investment, which is positioning nuclear as a differentiator in digital infrastructure and AI energy systems.

Innovation Meets Scale in Record-Breaking Deal Flow

The late-2020s are already setting records for nuclear fundraising, with investments boosting liquidity and valuations across public and private markets.

Pacific Fusion: $900M Series A

Helion Energy: $425M Series F (with tech firm agreements)

X-energy: $700M Series C-1

Newcleo: $150M Series A (HQ moved to France for EU backing)

A wave of data center deals and M&A activity is remaking the space:

BWX Technologies acquired Kinectrics ($525M)

Energy Fuels acquired RadTran (medical isotope supplier)

Startups like NANO Nuclear Energy and Oklo are going public—opening new institutional entry points. These transactions reflect major data center deals tied to nuclear infrastructure.

What’s Different This Time: Technology, Safety, Modularity

Innovation in Reactor Design

Small Modular Reactors (SMRs): NuScale, Deep Fission, and TerraPower

Microreactors: For remote, industrial, and extraterrestrial use

Advanced Fusion: Thorizon’s waste-to-energy and Marvel Fusion’s laser-driven systems

SMRs are becoming financeable, factory-built, and deployable solutions for clean energy scaling.

Waste Management & Efficiency

Breakthroughs in:

Closed fuel cycles

Dry cask storage

Waste-repurposing reactors (e.g., Oklo, Thorizon)

These are crucial for the long-term success of nuclear powered data center ecosystems.

The Financials & Market Opportunity

Market size: $204B (2022) → $271B (2027)

Capacity targets: 812 GW by 2050

Capex: $150B–$1.1T by 2050

Unit economics: ~$30–32/MWh LCOE

Institutional & VC Sentiment

From Breakthrough Energy Ventures to Founders Fund, top capital views nuclear as deep tech with upside.

The uranium market is resurging and drawing in global investors looking for scalable AI energy investment opportunities.

Policy + Private Capital = Alignment

State players (DOE, Rosatom, Westinghouse) are aligned with tech

Cross-sector pledges (e.g., WNA 2050 goal) gain traction

Legislation (ADVANCE Act) is fast-tracking deployments

Signals to Watch – and How to Invest

Follow the Data Center Giants

Their equity stakes are the blueprint for future nuclear powered data center expansion

Prefer Scalable Platforms

SMRs like NuScale, Deep Fission

Fuel-cycle firms like Oklo, Thorizon

Track Fast-Track Markets

U.S., France, China, UAE, and India are leading the way.

Tap the Financing Ecosystem

ETFs (URA), specialist funds (BNP Paribas), and institutional flows are supporting nuclear energy investments.

Conclusion: Core Infrastructure for the Next Decade

The era of greenfield nuclear investments is no longer speculative. For CIOs and sector strategists, nuclear is now a core pillar—especially for supporting the digital economy and the expanding AI data centre energy footprint.

Big Tech’s investment has already reshaped the landscape—and this is just the beginning.

Disclosure: This post draws from the latest research and transaction data generated by Wokelo AI Platform as of May 2025. No forward-looking investment recommendations are offered.

How Technology is Making Mental Health Care Accessible amidst a Growing Crisis

Reading Time: 6minutesA wave of innovation is making mental health care more accessible, personalized, and effective. From AI-driven platforms to teletherapy and digital therapeutics, this sector has proven itself to be more than a passing trend – with healthcare organizations, clinicians, academic bodies and investors converging on the opportunity, drawn by both a clear public need and strong commercial potential. Here are 10 key trends and takeaways that underline the potential and challenges within the mental health tech space. 1. Surging market growth: Mental health tech is here to stay The global mental health market was valued at $410 billion in 2023 with growth rate modest at 4%. However, the digital mental health segment is projected to grow at nearly 20% CAGR, from $23.45 billion in 2023 to $72.3 billion by 2032. The growth is driven by the increasing demand for more accessible, cost-effective, and scalable mental health solutions, particularly as global mental health crises, exacerbated by the COVID-19 pandemic, demand innovative solutions. This market expansion is not just about technological novelty but reflects the real, sustained demand for services. For example, Headspace, a leading mental health app, has already achieved over 80 million downloads and 2.8 million subscribers globally, while Calm […]

Reading Time: 6minutesA wave of innovation is making mental health care more accessible, personalized, and effective. From AI-driven platforms to teletherapy and digital therapeutics, this sector has proven itself to be more than a passing trend – with …

Reading Time: 6minutes

A wave of innovation is making mental health care more accessible, personalized, and effective. From AI-driven platforms to teletherapy and digital therapeutics, this sector has proven itself to be more than a passing trend – with healthcare organizations, clinicians, academic bodies and investors converging on the opportunity, drawn by both a clear public need and strong commercial potential. Here are 10 key trends and takeaways that underline the potential and challenges within the mental health tech space.

1. Surging market growth: Mental health tech is here to stay

The global mental health market was valued at $410 billion in 2023 with growth rate modest at 4%. However, the digital mental health segment is projected to grow at nearly 20% CAGR, from $23.45 billion in 2023 to $72.3 billion by 2032.

The growth is driven by the increasing demand for more accessible, cost-effective, and scalable mental health solutions, particularly as global mental health crises, exacerbated by the COVID-19 pandemic, demand innovative solutions. This market expansion is not just about technological novelty but reflects the real, sustained demand for services.

For example, Headspace, a leading mental health app, has already achieved over 80 million downloads and 2.8 million subscribers globally, while Calm boasts 130 million downloads and 4.5 million subscribers, showcasing consumer readiness to engage with digital mental health tools.

2. Artificial Intelligence is redefining diagnosis and treatment

The convergence of big data and machine learning has prompted the creation of advanced triage and diagnostic systems. AI-driven solutions, such as those from Brightside Health and Character.ai are enhancing diagnostic precision and delivering personalized treatment.

Brightside’s proprietary precision prescribing system has treated over 200,000 patients and secured $100 million in investment. Similarly, solutions like Deliberate AI’s AI-COA aim to refine mental health assessments by analyzing complex data instead of relying solely on patient self-reports. These AI systems are not only improving therapeutic outcomes but also reducing clinician workloads, making treatment more efficient.

AI’s role in mental health is moving beyond diagnostics. AI chatbots and virtual therapists, like Woebot and Wysa, are now mainstream tools in providing scalable mental health interventions.

3. Telehealth platforms are overcoming geographic and provider barriers

Among the most transformative solutions are the ones connecting patients to licensed therapists. Telehealth platforms like Talkspace and BetterHelp have removed geographical and logistical barriers to mental health support, ensuring quicker appointment scheduling over week-long waits for in-person therapy.

This is particularly significant in underserved areas where access to mental health professionals is limited. The global shift to virtual care post-pandemic has also driven the surge in mental health service bookings. As of January 2025, BetterHelp had crossed 5 million patients benefitting from their virtual therapy services.

Strategic partnerships further illustrate telehealth’s growing influence and viable scale. Talkspace has partnered with major organizations like Amazon Health Services to simplify mental health benefit access for 150 million eligible members.

4. Emerging digital therapeutics are reshaping treatment approaches

Digital therapeutics platforms, such as SleepioRx and DaylightRx, are gaining momentum as clinically validated, effective treatments that complement traditional therapies. These platforms use techniques like cognitive behavioral therapy (CBT) to treat conditions such as anxiety, depression, and insomnia.

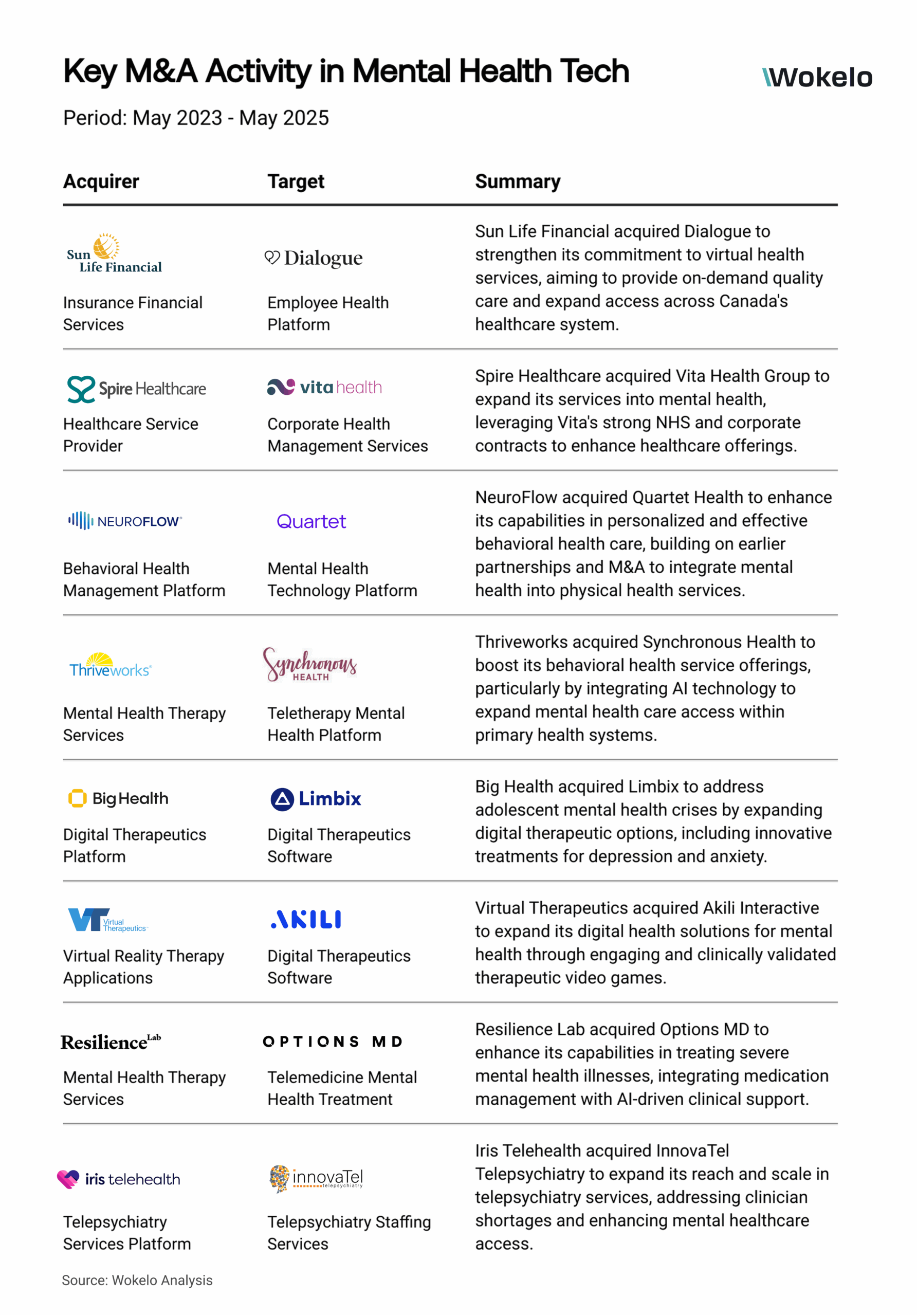

Investors are increasingly recognizing the value of these digital treatments, with platforms like Big Health acquiring Limbix to expand its digital offerings for adolescent mental health. The digital therapeutics segment is growing at a rapid pace and has shown significant promise in improving patient outcomes while lowering treatment costs.

5.Wearables are ushering in a wave of proactive detection and management

Wearable technology, such as the devices offered by Greenspace Health and Affiniti AI, is enabling continuous monitoring of mental health indicators like heart rate, sleep patterns, and physical activity. These real-time insights are crucial for providing personalized care and intervening before mental health conditions worsen.

The global wearable medical devices market is forecast to grow CAGR of 22–25%, with the potential to significantly impact how mental health is managed both individually and within healthcare systems.

Moreover, wearable integration with AI-driven platforms enhances the personalization of treatment, creating opportunities for proactive intervention and preventative care models.

6. Personalization for specific groups and their unique needs is key

Growing awareness of mental health challenges among teens, college-aged adults, and Gen Z has prompted mental health tech innovators to adjust their focus and offerings. Specialized solutions to reach these younger populations, as well as key demographics such as women and mothers are enhancing accessibility and providing tailored support.

Caraway’s mobile-friendly system merges mental, physical, and reproductive health features for Gen Z, while Blackbird Health uses neuroscience to target early youth interventions. The Child Mind Institute’s Mirror journaling app emphasizes trust, privacy, and guided prompts for teens.

Vita Health, meanwhile, serves at-risk teens and young adults with telehealth-based suicide prevention, expanding through value-based contracts. Talkspace has broadened its scope to support teens via phone-based resources and community forums and partnered with women’s health providers to address wider needs. By collaborating with schools, employers, and public initiatives, these tech innovators are accelerating adoption among populations that need it most.

7. Large healthcare actors and investors are backing the sector

An important factor fueling confidence in the market is the involvement of large healthcare corporations, credible clinicians, and academic bodies. Over the last few years, well-known hospital networks and healthcare providers have begun forming partnerships to integrate digital mental health into their practices, for example, collaborations for emergency virtual telepsychiatry for patients who need immediate intervention.

The increasing interest from major healthcare players and institutional investors signals that mental health tech is gaining mainstream credibility. Sun Life Financial’s acquisition of Dialogue, valued at $365 million, illustrates the growing interest in digital mental health solutions. Similarly, MPM Capital’s acquisition of Reunion Neuroscience demonstrates a shift towards backing mental health pharmaceutical and biotech innovations.

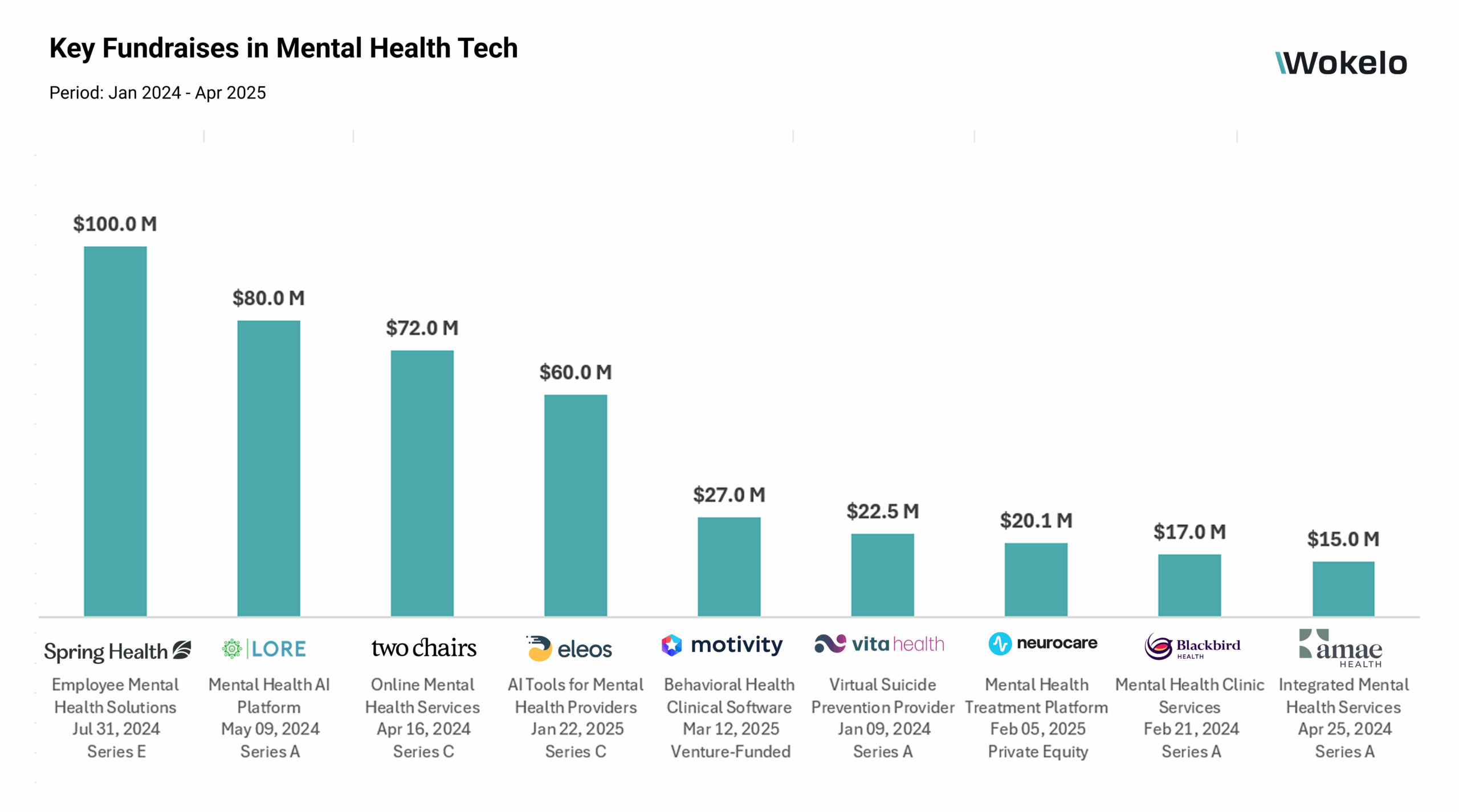

Companies like Lore, Two Chairs, Motivity, Eleos, Amae Health and Vita Health have secured multi-million-dollar funding rounds, showcasing confidence in both digital health and precision mental health care solutions.

8. Regulatory frameworks are evolving to support digital solutions

Digital health involves handling sensitive personal data, requiring careful navigation of frameworks such as HIPAA in the United States and GDPR in Europe. While supportive guidelines are emerging, the cross-border nature of digital platforms makes compliance an ongoing challenge.

Regulatory bodies are adapting to the fast-paced growth of digital health solutions. In the U.S., the FDA is developing frameworks for Software as a Medical Device (SaMD) and AI-powered tools, ensuring that mental health tech is both safe and effective for users.

Meanwhile, international initiatives, such as the UK’s MHRA and NICE guidelines, are shaping how digital mental health tools are evaluated for clinical efficacy. This evolving regulatory landscape provides a pathway for more widespread adoption, fostering investor confidence and enhancing the commercial viability of mental health tech products.

9. In this fast-crowding market, scale and adoption are critical

As the market for mental health tech matures, competition is intensifying. Established players like BetterHelp and Talkspace are facing competition from a wave of new startups such as Woebot Labs, which utilizes AI to deliver CBT, and Greenspace Health, which integrates data-driven measurement tools for improved clinical outcomes. and companies must differentiate themselves through innovation and evidence-based outcomes.

Digital platforms are also integrating with traditional healthcare systems to drive adoption. The collaboration between TeamHealth and Array Behavioral Care is a prime example of how technology can help traditional healthcare systems to address clinician shortages, while the large healthcare networks can help adoption of digital solutions.

Similarly, Spring Health’s partnership with employers and universities to provide AI-driven mental health solutions further demonstrates how tech companies are reaching wider scale by embedding their services into the workplace and other institutions.

10. Data privacy and security remain critical for consumer trust

Because these tools capture intimate emotional data, robust encryption, secure data storage, and transparent user consents are essential. Any breach of trust could hamper adoption. Data security concerns continue to be a significant barrier for consumers, with 73% of mental health app users stating that data misuse concerns would cause them abandon the app.

However, companies that prioritize strong data privacy protections have experienced up to a 40% increase in user retention. Compliance with regulations such as HIPAA and GDPR is essential for companies looking to build trust with users and ensure the long-term success of their platforms.

As mental health tech becomes more integrated into the mainstream, prioritizing consumer privacy and ethical data management will be key to overcoming skepticism and driving broader market adoption.

Conclusion

A key argument for investing in mental health technology lies in the potential to reach vast consumer segments rapidly. Traditional face-to-face therapy often struggles with backlog and cost constraints, while digital solutions can scale seamlessly. Beyond just teletherapy appointments, digital solutions can integrate self-monitoring tools, asynchronous messaging, and AI-based clinical decision support – models that have seen proven success and traction in the physical health segments.

Although total funding in this space dipped recently, the market’s projected growth rates underscore a strong commercial outlook. Many large healthcare insurers and systems continue expanding digital behavioral health coverage, while employers increasingly treat mental health as an extension of standard medical benefits. Government interest and academic involvement also indicate that mental health solutions are no longer peripheral in healthcare policy debates.

For prospective investors, the opportunity is twofold: first, to back technologies that could become indispensable in mainstream mental health provision; and second, to drive social impact by facilitating broader, more equitable access to vital support.